Standing Fast in Japan

[Update on the recent data added below]

Being a BOJ watcher can indeed be a tough job in terms of forecasting but sometimes it is also pretty easy. Consequently, the BOJ chose today, pretty much as expected, to hold rates steady on the back of a return of deflation in the recent months and also I guess on the back of the outlook that deflation will persist in Q1 07 and perhaps even well into Q2 07 as well. Also of course the slowdown in the US which after all is Japan's biggest export market.

The Bank of Japan kept interest rates unchanged for a second month after consumer prices fell and recent data signaled U.S. economic growth may slow.

Governor Toshihiko Fukui and his policy board colleagues voted unanimously to hold the key overnight lending rate at 0.5 percent, the lowest among major economies, the bank said in a statement today in Tokyo. The decision was expected by all 49 economists surveyed by Bloomberg News.

Fukui later told reporters that the U.S. economy will achieve a soft landing and Japan's consumer prices will rise in the long run after hovering around zero percent in coming months. Confidence among Japan's largest manufacturers slipped from a two-year high on concern a U.S. slowdown may hurt exports, the central bank's quarterly Tankan business survey showed last week.

``There's still a pretty big chance for a rate hike later this year if the central bank can confirm Japan's growth is supported by demand at home, even if the U.S. economy deteriorates,'' said Ryutaro Kono, chief economist at BNP Paribas Securities Japan Ltd. ``We expect the bank to act in the fourth quarter.''

For more on the outlook on the Japanese economy you can check out my recent notes which also dicusses in more detail the outlook in deflation based on recent analysis by Takehiro Sato from Morgan Stanley. More interestingly, we have consumer spending which indeed has shown positive signs as of late and most likely will show a healthy growth clip y-o-y in %. However, remember still that 2006 was a below trend year in terms of consumption expenditure and that consumption expenditure is still below 100 on a real Index 100 (2005) basis. In fact the trend since 2000 is one of secular decline as shown in the figure below.

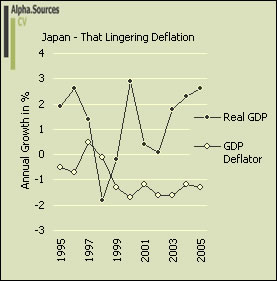

This of course does not mean that this might not signify a significant pick-up but my main worry is that deflation will entrench itself in Q2 of 2007 which could feed into expectations and since Japanese consumers already are saving a lot the pick-up in consumption expenditure will perhaps be shortlived. For sure, the chance of a y-o-y improvement is there but I do not see a change in the overall trend. Finally and on deflation I leave you with a chart plotting real GDP growth and the evolution of the GDP deflation since 2001. As you can see real GDP has picked up as of late but of course so has a the Japanese trade surplus.

On a very last note I am not chaning my main position here and the outlook on deflation still worries me most although of course the recent pickup in consumption expenditure is most welcome. In terms of interest rate decisions we should expect the G7 ministers and other high lords to pounce on Japan again come next weekend although I expect that the criticism will be less pronounced than last time. I do expect however that European G7 members and officials in particular will spend time on the Yen. However, I do not see the BOJ raising on this side of Q3 with the current outlook in deflation.

The recent data on manufacturing orders in Japan actually seems to require a revision to the downside of my call on capex spending in Japan in Q1 2007. Consequently, machine orders fell 5.2% in February which clearly suggest that exports are losing steam going into 2007 and since the US after all is the biggest export market (22%) then this might be a sign of a transmission mechanism in the works (de-coupling anyone :)?). This also means that industrial production most likely will have continued its decline in March and April on two accounts Firstly, as a result of de-stocking on the back of high capex in Q4 2006 and secondly, as a result of a real decline in foreign capacity proxied by a US slowdown and perhaps also a cooling in Chinese investment.

A second data piece on Japan which caught my eye was the news that corporate credit growth supplied by Japanese banks fell in March. The decline was, it needs to be said, ever so slight and corporate credit is still growing albeit more slowly it seems. This is of course likely to be a derivative of the points above and an indication that capex in Japan is slowing on an overall basis in the beginning of 2007.