Other Alpha Sources (Academic Version)

If you ask the layman about what economics is the answer you get is likely to contain the notion of money. This is understandable. After all, if economists do not study money in some form or the other what are we doing then?

As such, you might be surprised to learn that in the grand sweep of the economic literature, economists have often found it very difficult to explicitly model the role of money and indeed to incorporate this role into the overall model framework. Put very generally, graduate econ students will see two types of models which incorporate money. The first is the money in utility model (MIU) where money is simply added, alongside consumption, to the utility of the representative individual and where some form of monetary instrument (e.g. bonds) are added to the wealth and thus inter the problem through the budget constraint. The other is the cash in advance model (CIA) where we essentially assume that consumers must hold cash solely for the purpose of buying the goods that they want. Or in more convuluted terms; to facilitate the exchange of goods and services.

If the story above is the one that trickles down into the the university classroom the real world is of course more complicated and any student who starts to dig deeper will find a diverse literature which, notably, have been greatly enriched on the back of the financial crisis.

A paper from the Chicago Fed by Ed Nosal, Christopher Waller, and Randall Wright takes a look at recent endeavors in this field.

The first question which you would probably like to ask is; why the neglect by economists of money and the explicit modelling of something so important? Well, in the word of the authors, blame it on the general equilibriumnistas;

The reason many economists either ignore institutions like money, or slip them in with short cuts, is this: they do not take seriously the nature of the process of exchange. Following classical general equilibrium theory, agents do not trade with each other, but trade only against their budget constraints. Any bundle that is worth no more than the value of ones endowment is available, with no discussion of how it is to be acquired. Everyone worth his salt understands that there is no role in Debreus frictionless paradigm for money, intermediation, or anything else that facilitates the process of exchange since this process is not part of model.

But this is not the whole explanation (fortunately). As the authors go on to explain, many economists sees the working of money as the plumbing behind the scene and thus that it should be assumed to simple do its work (i.e. facilitate the exchanges in a Arrow-Debreu GE world). However, as the authors point out; what happens when the plumbing goes wrong? Indeed, what happens when liquidity, credit and ultimately money transmission mechanisms breaks down?

Some have argued that modeling the details of exchange and intermediation is nothing more than studying the plumbingof the economy it all works well behind the scenes and so we do not need to pay attention to it. This seems wrong. How do we know it is working well if we do not pay attention to it? What happens if the plumbinggoes bad? We know what this entails, and it is not pretty. We believe that it is dangerous to ignore the details of plumbingand that the recent nancial crisis makes this obvious. We therefore think that it is important to study institutions that help to facilitate exchange, and the papers in this special issue do just that.

And here then is the cue to go read the paper or at least to bookmark it. Note in particular how the authors group recent contributions in the context of money, credit and liquidity and thus what was originally simply a facilitator of exchange has now become a much broader concept.

Naturally, economists of an Austrian pedigree have known this for a while and one decidedly fruitful consequence of the financial crisis is the nascent incorporation of their thoughts into the mainstream economic methodology [1].

---

A lot has been written about Japanese savings and especially about when they would run out so as to make the country dependent on foreigners for the financing for the ever growing mountain of public debt. I have written extensively about this basically arguing that while the flow of savings in Japan is indeed inadequate for the ongoing financing of the debt, Japan has two things in their favor. The first is a large stock of domestic savings of which not everything, yet, is parked in government bonds and secondly, central bank which will be forced into taking up any bid that would otherwise have gone to yield hungry bond vigilantes.

A recent working paper by Tokuo Iwaisakoy and Keiko Okadaz from the Japan Ministry of Finance Policy Research Institute (PRI) looks to be well worth reading; (my emphasis);

The decline in Japans household saving rate accelerated sharply after 1998, but then decelerated again from 2003. Such nonlinear movement in the sav- ing rate cannot be explained by the monotonic trend of population aging alone. According to the life cycle model of consumption and saving, popu- lation aging will increase short-run uctuations in the saving rate, because the consumption of older households is less sensitive to income shocks. Ana- lyzing income and spending data for di¤erent age groups, we argue that this is exactly what happened during the recession following the banking panic of 1997/98. Two important changes in income distribution are associated with this mechanism. First, the negative labor income shock, which in the initial stages of the lost decadewas mostly borne by the younger genera- tion, spread to older working households in the late 1990s and early 2000s. Second, there was a signi cant income shift from labor to shareholders asso- ciated with the corporate restructuring being undertaken during this time. This resulted in a decline in the wage share, so that the increase in corporate saving o¤set the decline in household saving.

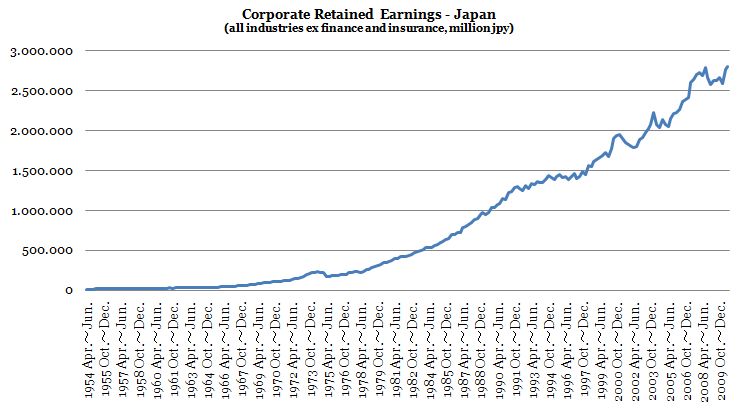

An important aspect of Japan's economy is the ongoing increase in corporate savings which is just about the only chart on the Japanse economy (apart from the public debt to GDP one) going up. Indeed, it may just be one of the most important charts to understand Japan's economy;

(click for larger image)

Retained earnings have grown at an average of 4% since 2000 and has thus offset, to a large extent, the decline in private household savings.

---

[1] - Indeed Austrians seem have become more mainstream in the aftermath of the financial crisis as a whole. This is no doubt to their great lament since it means you actually have to provide policy advice and not just advocate eternal damnation and bloodletting.