it's getting difficult to avoid the clichés

Cliché: a phrase or opinion that is overused and betrays a lack of original thought.

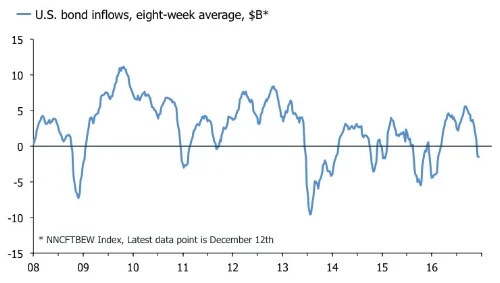

I wonder how many fixed income strategists had the famous exchange between Goldfinger and Mr. Bond in mind when they penned their missives this week. The Fed came and went, erring on the side of hawkishness, and bond holders once again found themselves at the front of the queue for the proctologist. U.S. yields surged across all maturities, adding fuel to the story of a regime change and genuine reflation story under the leadership of Mr. Trump. Trying to pin the U.S. bond market down in a few charts is not easy. Last week, I noted that my valuation scores suggests this is a good time to add exposure, but also that stock-to-bond returns, while high, weren't yet extreme. That situation has not changed even with last week's rise in yields. It is the same if we look at flows. The chart below shows the eight-week average of U.S. bond inflows proxied by the ICI net new cash flow into bonds. The latest value is December 9th, but even assuming a further lurch lower last week, it isn't extreme yet. What is extreme, however, is the COT net short speculative positioning—non-commercial—on U.S. 10-year futures. The net position crashed to -0.317M contracts based on the latest data from December 13th. That is an all-time record net short.

Time to add to fixed income?

That said, last week's carnage in bonds prompted yours truly to add some fixed income exposure in the portfolio. I was particularly interested to see the surge in U.S. 5-year yields. If we are indeed late cycle, it stands to reason that the Fed's hiking cycle—in response to a surge in fiscal stimulus—could be aggressive, but also short. That would suggest 2s5s flattener, and a 5y at 2.2% is pretty juicy in this regard. This is to say, if the U.S. economy faces a traditional monetary policy driven recession—not necessary a financial crisis—in the next 12-to-18 months, there is little chance that the Fed fund rate will be at above 2% on a five-year horizon. At least, I think the market is very aggressive in assuming that this will happen in a linear fashion.

The risks to dipping your toe into the shark-invested duration waters at the moment is obviously that the regime change in bonds are real. But even if equity bulls' wet dream of a structural rotation out of bonds into stocks plays out, the added benefit here is that stocks and bonds will be inversely correlated. If that is true, it means that buying fixed income and stocks on relative weakness is a good idea in itself. This assumes of course that you don't want to go full retard 120% long equities with no cash/bond position.

The macroeconomic evidence for the great reflation also is dubious. Sure, inflation and wages—at least in the U.S.—are accelerating, but these are lagging indicators, and their comeback simply adds to the evidence that the business cycle is long in the tooth. Assuming their rise comes with tighter, or less loose, monetary policy, how will it impact the parts of the market that have been piling on debt and risk exposure on the assumption that rates would never rise? I am not sure that I want to put all my eggs in Mr. Trump's basket to find out, at least not in the short run.

The next two charts show headline leading indices in the U.S., the EZ, China and Japan. The recent jump in global manufacturing surveys mean that the November/December update of these likely will look much better. But none of them are screaming accelerating growth.

What reflation?

Is Asia picking up momentum?

In the U.S. the NBER's leading indicator is growing a mere 1%-to-1.5% year-over-year, and in the EZ the momentum is an anaemic 0.4%. These indices are far from perfect indicators of GDP growth. Consumer sentiment in the U.S., for example, suggests that household consumption will accelerate soon. In the EZ, business and consumer sentiment suggest that GDP growth will remain above trend in the short run. But it adds to the idea that maybe the market has run a bit ahead of the Trumponomics story. The dramatic change in Chinese inflation data, however, is important. Factory gate price inflation in China has surged recently after being stuck below zero on a year-over-year basis since 2011. Base effects are part of the reason, but it injects an important element of change into the global inflation story. If sustained, it makes sense that bond yields should be higher, although how much higher is an entirely different question.

The dollar; will she, won't she?

When the world's largest and most liquid bond market moves, other asset markets follow. Last week's surge in the dollar is a case in point, a move which incidentally is a lay-up if you look at the likely policy mix under Mr. Trump. Loose fiscal policy in a late-cycle economy—where inflation already is rising—and tighter monetary policy on their own are conducive for a stronger currency. But in combination with other major central banks stuck at the zero bound, and conducting QE, it is like throwing kerosene on a fire. EURUSD at parity and USDJPY above 125 are now well within the realms of possibility, and in the most basic sense it is a story of monetary policy divergence. Consider for example that the Bank of Japan apparently is committed to a symmetric defence of its 0% 10-year yield target, despite the fact that if they let it run higher they might actually get a steeper yield curve. This suggests that the original interpretation of the BOJ's "yield curve control" was wrong, but it also points to a USDJPY that is completely unshackled. In other words; if the BOJ intends to keep its bond market isolated from any second-round effects from Fed tightening, they will need to print a lot of JPY to back it up. In the Eurozone, the chart below shows the 10-year yield spread between the U.S. and Germany, which has recently blown out to a level not seen since the 1970.

A regime change in global bond yield spreads?

So far so good then. Staying on the dollar-strength train makes sense from the point of view of wider global interest differentials. But a strong dollar also represents a bit of a macroeconomic conundrum. On the one hand, it could part of a package that pushes global growth to a pre-2008 pace. The dollar strengthens, the U.S. C/A deficit widens, and the rest of the world finances Mr. Trump's plans of reviving the U.S. rust belt and manufacturing. The global FX stars are almost perfect aligned for this theme at the moment. EM FX is weak, the Yuan almost surely would suffer if it free floated, the GBP is under the weather due to Brexit, and the euro and yen haven't really changed. If the U.S. lets fly with tight monetary policy and aggressive fiscal easing, it would be a recipe for Bretton Woods II^2. On the other hand, Mr. Trump and his new administration have specifically said that they want to clamp down on currency manipulators, which presumably means sticking it to economies that run excessive external surpluses with the U.S. economy. Mexico's access to the U.S. market via NAFTA is under serious threat, and China likely will have the dubious honour of being labelled a "currency manipulator" immediately after Mr. Trump is inaugurated. If that turns out to be order of the day, my decision to buy bonds likely will turn out to be a mistake. A policy mix of looser fiscal policy, tighter monetary policy and clamping down on foreign trade is a recipe for an inflation bon-fire. In any case, how the new U.S. administration chooses to balance its objectives on this matter is probably the most important question for investors to gauge at the moment.

Nothing but upside in equities?

Equities were rather uninteresting last week compared to the price action in other asset classes with the MSCI World and Spoos finishing down a modest 0.3% and 0.1% respectively. This gave respite to the bears, which suffered a beating the week before, but probably didn't deter the bulls. In last week's missive I showed the extreme put/call ratio on the S&P 500, and mused that it was signalling pain ahead for the longs. Well, guess what ... it got more extreme last week.

Go buy some calls, I dare you

It certainly appears that it will struggle to move much further to the downside here, which again indicates that call buyers might kick from the table soon. But does it actually signal anything. To find out, I conducted a little study. The chart below shows the instances when the put/call ratio z-score has been below -2 and trailing S&P 500 returns have been above 5%, which pretty much replicates the situation we are in now.

Time to sell?

Optically it looks decent in terms of catching short-term drawdowns, but a sample size of four isn't exactly statistically significant. It gets worse after the backtest. The average two-week, 1m and 3m returns after the signal are -0.1%, -1.4% and +0.5% respectively with the entire negative contribution due to the perfect catch of the sell-off in 2008. Take that out, and the market should rise based on this signal. That conclusion is obviously incredibly annoying, but illustrates the pitfalls involved in trying to capture the short-term twists and turns in the stock market. In any case, punting Spoos was never my game, so I am content with the secondary conclusion from this little exercise: There is absolutely no need to chase the market here, or pile into single positions on the long side.

The final story I wanted to highlight in equities this week is the significant improvement in breadth on the Eurostoxx 50. The chart below shows that the number of stocks making new highs on a 52w basis has surged recently, which signals that the bear market in EZ equities is over.

Is the EZ equity bear market over?

That is some assumption of course, but stay with me. We know that the depression in financials have been the key driver of underperformance of EZ beta, and we know that these stocks have recently jumped. In other words; if EZ beta is going to continue doing well from here, it has to rely on financials. I know that sounds incredibly unappealing, but it is the true contrarian bet at the moment. After all, I am sure you remember those DB/Lehman overlay charts hitting the headlines earlier this, and that didn't work out so well. Sometimes, however, contrarian investing—like using old movie scenes as metaphors for trading themes—can be too much of a cliché.

--

Sorry for the "hanging" sentence at the end. It has now been removed.