Random Shots - Return of the Deflation Trade?

I recently asked the opnion of my readers regarding the question of whether the global economy is in for inflation, deflation, or stagflation. Given the obvious issue that it may be all three at different points in time it seems as if recent market action suggests that we should be looking at the d-word.

QE1 + QE2 +...+QEn = Deflation?

Even if macro soothsayer's favorite comparison between Japan and the US is misleading because the former has decidedly more miserable demographics than the former, it is clear that US policy makers are steering into largely uncharted waters.

Consider then Atlanta Fed President Dennis Lockhart's recent comments before the National Association of Business Economics that the Fed would contemplate cueing in QE3 in the event that the current oil price shock proved to be more severe. On the face of it this makes sense in so far as goes the idea that the main effect from sharply rising oil price is a relapse into recession and thus deflation. Indeed, the Fed can hardly be blamed for acting in the context of events which are essentially geo-political in nature.

Yet, it is much more complicated than that.

It then stands to reason that while the Fed should certainly be forward looking in conducting policy the primary effect of ongoing measures of quantitative easing is exactly to put pressures on headline inflation and commodities in general. As I noted recently at this space;

Given that we seem to be looking at a re-run of 2008 it must be factored in that the volatility and speed (and subsequent decline) of commodity prices are a problem in itself. The famous loss function which must then be metaphorically minimised is the one which plots the trade-off between the cost of recurrent flares of commodity prices and the need to act as a counter trend to the destructive forces of a balance sheet recession. Here, it becomes a rather serious issue if one of the main collateral effects of providing buckets of liquidity is to engender strong commodity melt-ups with a subsequent deflationary outcome.

And perhaps this is what is running through the mind of Dallas Fed President Richard Fisher who, in the same picece as linked above, is quoted of voicing oppositon towards QE3 and indeed that he would like QE2 to be phased out sooner rather than later.

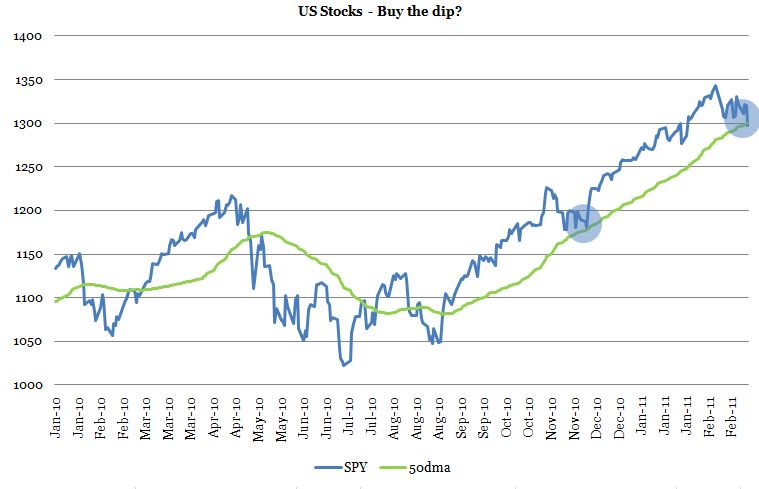

Which way the tide will turn at the Fed is not a trivial question. There are plenty of signs that after the SP500 having tested the 1350 level, and failed, the market is running on the evaporating fumes of QE2. As one of my many market spies noted today:

(...) it is definitely possible that the market will discount the end of QE2 ahead of time this time around. This is what happened in Japan too - the market began to rally as soon as their QE2 was announced (since it had rallied smartly on QE1) , but halfway through the implementation the Nikkei began to fall, ultimately losing 45% from the interim peak and ending below the level of the day QE2 was announced. Mind, I'm not saying it will play out in the exact same manner, this is just to point out that there can be leads and lags between QE and its effect on the stock market - the QE1 experience is not necessarily a road map that needs to be repeated.

Again, we have that comparison with Japan which is then only to say that repetitions in the market rarely occur the way you expect them to, but there is definitely an unwinding narrative emerging. Team Macro Man gives their list of bearish omens today and I find it difficult disagreeing with them on the general idea that the reflation trade might be in for a stutter; at least until the next round of QE.

To their list I would add that another favorite punt of the reflationistas, gold, is finding it mightly difficult to reach new highs above the 1420s (today, Thursday, getting a right beating back to 1405ish). Now, we should always remember that the market can move three ways, where sideways is the third. Yet, the fundamentals of the gold trade kind of black or write so the ongoing difficulty reaching new highs will be rightly worrying the g-bugs.

More generally however the SP500 is only now coming down to the 50dma (at pixel time) and I would wait to see whether it forcefully breaches that level before putting on the tin foil hat.

(click image for better viewing)

As you can see dear reader, the chart is telling you to buy the dip, but chartism on such short time scales can make plenty of widows too, so be careful out there.

Looking into the rearview mirror at the ECB

I wasn't really sure whether to cry or laugh last week when Trichet mounted himself in front of the microphones to deliver an almost sure signal of future rate increases by invoking the idea of strong vigilance. Indeed, the ECB let it be known that it was perfectly possible that their April meeting would be accompanied by a rate increase. Game set and match then!

As I have noted before at this space, stranger things have happened than the ECB raising rates just before a global slowdown. I even ventured to call it a leading indicator. Soc Gen's always enjoyable Albert Edwards dryly noted recently (HT: FT Alphaville); “all we need now to push the world back into the recession is an ECB rate rise.”

This seems an apt take on the situation and my good friend Edward Hugh similarly notes that all this has an alltogether well expected outcome invoking the idea of the Chronicle of a Policy Error Foretold.

Now the problem with this latest policy initiative is not only that it represents something akin to the chronicle of an early death foretold for a much troubled and highly fragile Spanish economy, where around 90 percent of mortgages are variable rate ones.

It also draws attention to an area which it would be much better for the ECB not to draw attention to at this delicate moment in its history: the convenience of having a single-size monetary policy applied to such a diverse group of economies.

I heartily agree that it is due time that we, yet again, try to evaluate what it means to have a single interest policy in the eurozone. More specifically, there is the question of divergence of fortunes when it comes to deflation and inflation;

Inflation on the periphery has much more to do with rising commodity prices and the application of a misguided policy of consumption tax increases as a way of reducing fiscal deficits than ever it has to do with economic overheating.

I think it is pretty obvious that there will be no second round effects in the eurozone periphery and if the ECB is seriously suggesting this to be the case, I would dearly like to see the empirical evidence for such a claim (even a theoretical would do actually!).

Finally, we should never neglect to mention that all this might be a bluff and that the ECB like most other rational institutions can change direction based on the evidence before them. Yet, herein also lies the rub because the current vigilance comes on a backdrop which smells a lot like the last time the ECB raised only to see the deck of cards fold before their eyes. Perhaps they ought to look closer into the rear view mirror.

Random Shots indeed

The immediate conclusion here would seem to be that Trichet should get on a plane and relieve Bernanke of his post in Washington and leave the tower of Frankfurt to Benny. As FT Alphaville (see link above) quotes from Gavekal;

Since its inception, the ECB has typically been slow to cut rates (famously rising them in July 2008!) and slow to raise them. So is the fact that the ECB is now considering a tighter monetary policy before the Fed a sign that the ECB is making a mistake? Or a sign that the Fed is starting to really fall behind the curve?

I am not sure that it is either really. Core inflation in the US is still nudging down but I think that ongoing loose monetary policy will run the risk of replicating the UK more than Japan. Put differently, I think the US economy is in a position where inflation expectations might take hold which is not the case in the Eurozone periphery at large.

At the time of writing it seems an awful lot as it the deflation trade is back and thus that the market has already sucked QE2 dry and now awaits the third version. A spike in oil prices helps no-one too, but oil at current levels is not the problem, but a quick zoom to 150ish and we would have grave problems. This would then be ample catalyst for QE3 and even if this would not prevent the correction which seems evident now, it would setup another meltup in all things unprintable and risky.

We can only hope then that central banks, on either side of the pond, are taking more than random shots at our current problems.