Random Shots

(click pictures for better viewing)

It has been a while since I have had a round of these and in the current macro/market environment I thought it an excellent occasion to take some pot-shots at the market discourse. So, read on if you want to see what it looks like when I am being (excessively) smug, an econometric model of Eurozone industrial production (no shit!) and a look at them US treasury yields which have gotten an awful lot of attention lately.

Don't ya just love it when you are right?

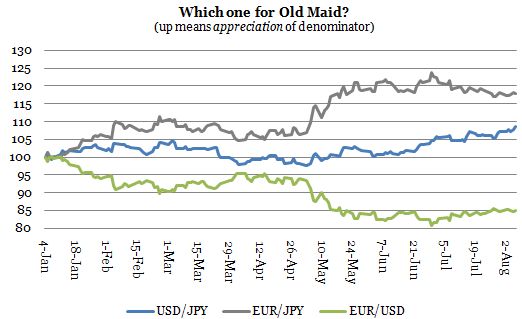

Well I do and while this is not making a killer profit kind of right I still take comfort in the fact that the themes I am talking and thinking about also seem to be moving much closer to the center of the financial market discourse. First off, do you remember my notion of the Old Maid in the context of G3 currency markets?

Old Maid is a card game where the simple task is to avoid holding a given card (often the queen of spades) at the end. Even in the company of good friends however, holding Old Maid at the end is not fun. Often, you have to buy the drinks, drop a piece of clothes, or endure other travails. And as it turns out, the global FX market is not unlike this good old game of cards where the Old Maid is proxied by having a strong currency on whose shoulders the correction of global macroeconomic imbalances must invariably fall. In this way, and although one sometimes get the feeling that everyone believes that everybody may actually export their way out of their current misery, buying one country’s currency means selling another and thus, someone (be it an individual economy or a group/basket of economies) must end up holding Old Maid.

I hope the, albeit convoluted, introduction above will give you an idea of where I am going with this. Never mind of course that I was not entirely right in terms of which currency that would turn out Old Maid since I predicted the USD to strengthen (it has against the Euro) consistently in 2010 and while I believe this to come through eventually, the story so far has been a bit more complicated. First off, the USD did start 2010 holding Old Maid as tensions in the Eurozone saw the Euro plummet, but contrary to expectations, the remarkable strength of the JPY is becoming a story which cannot be ignored; in particular, its ill-recovered role as safe haven currency of choice in times of risk-off sentiment is something I did not expect.

To that end I feel vindicated in my overall theme and as such I welcome the Economist on my side of the fence as they articulate, this week, the idea of a race to the bottom among G3 currencies. I like the following in particular;

A cheap currency is especially prized now, when aggregate demand in the rich world is so scarce and exports to emerging markets seem the best hope of economic salvation. (...) The battle for a cheap currency may eventually cause transatlantic (and transpacific) tension: not everyone can push down their exchange rates at once. For now, though, the dollar holds the cheap-money prize.

Now, I am ready to repeat this almost to the degree of my readers potentially reaching insanity; the G3 are now effeftively dependent on exports to grow and since they are all looking to the same customers you end up with too much supply (of savings) relative to demand. Or ... we can turn it around and say that there is too much demand for yield (excess supply of savings) relative to supply (capacity to absorb it). See, this is not so difficult.

The important part of course and where it all comes together is that this export dependency/propensity to save is not a deus ex macina but has a concrete and real driving force. In that vein, two recent contributions to the debate are very important. First off, we have Előd Takáts' BIS paper on ageing and asset prices which provides evidence to show how ageing, in the context of real estate prices, are deflationary [1]. Now, I might take issue with the theoretical framework being a life cycle and not a life course model (wonk alert!) and I might also take issue with the empirical framework, but I wholeheartedly support the paper's conclusion.

The estimates show that demographic factors affect real house prices significantly. Combining the results with UN population projections suggests that ageing will lower real house prices substantially over the next forty years. The headwind is around 80 basis points per annum in the United States and much stronger in Europe and Japan. Based on the analysis, global asset prices are likely to face substantial headwinds from ageing.

Note here his sample is only the OECD and thus global is somewhat a misnomer here.

Secondly, I welcome no other than almighty Goldman Sachs on my side of the fence (hat tip FT Alphaville) with their recent exposition on how global imbalances might not actually get better, but worse, and how all this is down to demographics.

Up to the age of 35, the population appears to be a drag on the current account position—in other words, people invest more than they save, on average. Between ages 35 and 69, people on average appear to save more than they invest. These are the so-called ‘prime savers’, and having more of them in the population would tend to improve the current account position ...

In Alpha.Sources land this is a well known tune and while it may actually be a little more complicated than this I find it extraordinarily refreshing to be arguing alongside the Illuminati in the future. Now, I should make it immediately clear here that Goldman's final conclusion is problematic;

These shifts could push towards a cleaner split between EM (mostly in surplus) and DM (mostly in deficit) than is the case in the current, more complex picture. In particular, demographic pressures could see the largest DM surplus countries (Japan and Germany) move into deficit and the largest EM deficit countries (Brazil, India and Turkey) move into surplus.

Well actually, they are just plain wrong here. Basically, they are scratching in the right places but end up with the wrong conclusions because they neglect the effect from ageing on aggregate demand. The argument above hinges on a link between dissaving and external deficits which is difficult to reconcile with rational economic behaviour. Finally though, and as a perspective I have only recently started to think about the role of (lagged) capital deepening in emerging markets is very, very significant as well.

What about that double-dip then?

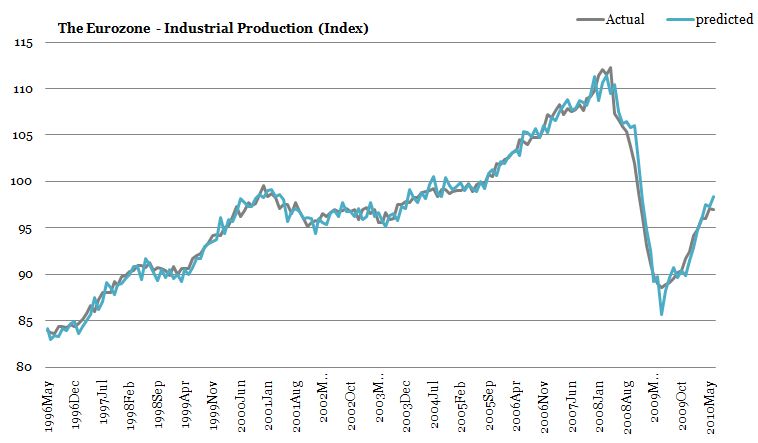

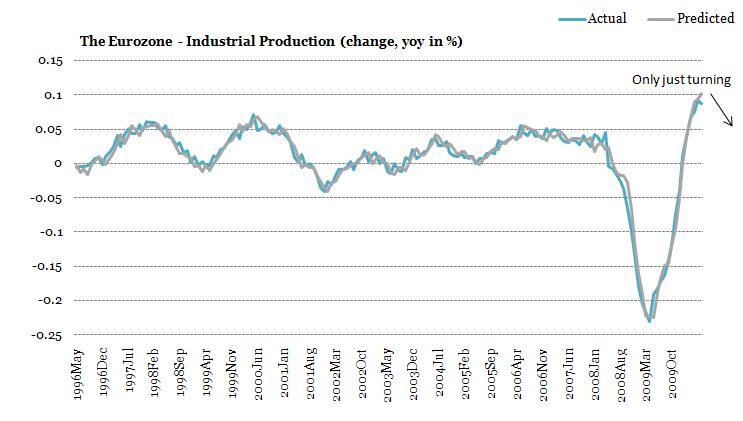

So, Eurozone industrial production took a turn for the worse in June with the drop driven by weakness in durable consumer goods such as furniture and home appliances according to Bloomberg. To that end I thought that I would try to asses the potential for a double dip (in Europe) based on Alpha.Sources' (only) proprietary econometric model.

I remain bearish on the macro environment in Europe and indeed I think that deflation will ultimately be a continent wide outcome, but timing is of the essence here. We learned today that Germany put in an all time excellent economic performance in Q2-10 which does indeed seem to be paving the way for a downward turn in H2 2010 (especially since my guess is much of this was driven by inventories). This view is somewhat supported by the evolution in industrial production which seems to be signalling a turning point in the annual change. This is consistent with mean reversion of the index in annual changes and, in economic terms, with a slowdown in momentum. This is interesting as the turning point would occur at a point where the level of industrial production was still some 10-15% lower than pre-crisis peaks and indeed still lower than in 2005 (2005 = 100 in the charts above).

Further evidence today comes from the overall Flash estimate of Q2-10 European GDP which shows that Germany remains the only real stellar growth story. Over the quarter both EU27 and EU16 grew an impressive 1.0% driven by strong growth rates in Germany and France. Greece on the other hand saw its contraction accelerating and over the year both Greece and Spain saw contractions (Spain saw a 0.2 expansion over the quarter).

In this sense, European growth remains very skittish and I think we will see a double dip in the Eurozone in H2-10 while the US should just avoid one. Finally, I maintain my view that although growth will slow to the detriment of risk assets, there is almost no risk of a global double dip due to continuing strong growth in Asia and Latin America.

Where goes them US treasury yields?

Probably the most hotly debated lately has been the relentless decline in US treasury yields and by extension the idea that deflation has become an entrenched reality at the same time as stock markets have soared. Now, there are a lot of ways to skin this cat which should be evident on the basis of the absolute storm of punditry on this issue lately. A couple of important general points are worth mentioning here. First of all, this is closely tied to the the prospects of a double-dip recession in the US where some commentators have recently flagged the issue that while conventional recession indicators point to sustained growth these very same indicators rely heavily on the slope of the yield curve (e.g. Albert Edwards from Soc Gen and BCA have recently made this point in their research). The point is that since short term rates (and by derivative yields) are already close to zero there is no way that the yield curve can invert (a traditional harbringer of recession) even if a recession is imminent. Secondly, it would be nice to be able to argue on the basis of some simple arithmetic rule here such as e.g. mean reversion, but the problem is that even when deflated by the annual change in CPI the real yield on US treasuries (2y and 10y in this case) are still trending (downwards).

I will neatly sidestep any discussion about whether this is end of the bull market in government bonds since this is a chicken-and-egg type of discussion. If you believe in perma-deflation, short term yields will hover around zero and, c.f. the latest from Rosenberg, the Fed will try flatten the yield curve by moving in on the long end. I am leaning towards this scenario for 2011 and thus lower yields are here to stay (at least in nominal terms). If we take the current message from the 2y and 10 year yields at face value and assume, naively, that the average inflation rate for 2010 will prevail as an average over the next 10 years the outlook is poor with real yields on the 2y notes negative and only slightly positive for the 10y horizon. Going back to Rosenberg, what he is essentially saying is that bringing on additional QE might serve to flatten yield curve from the long end of the spectrum as the Fed begins to massage yields at longer maturity.

Indeed, as a result of record low yields on 2y notes the 10y2y curve has never been steeper than is currently the case and while we would expect short term interest rate to flatten it as we move into recovery, this time might be different (going back to Rosenberg's argument again even though 10y is not long term in the ultimate sense of the word when talking about treasury yields).

So where do they go? Let me answer that question with another (rhetorical) question. Do I believe that QEI, II, III etc will work and ward off deflation in the US? Yep, I do and as such I see higher yields going forward, but for now I am very comfortable with the call that short term yields will remain low for at least the next 12 months and that Rosenberg is likely to be right. So, not quite time yet to take a random pot sho(r)t at them bonds.

---

[1] - Link this to the notion that global imbalances are driven by real estate price fluctuations and housing market dynamics and you should have that fuzzy feeling by now.

Data is from the ECB and FRED (St. Louis Fed)